Behaviourally, it’s been shown that investors value a company that pays regular dividends more highly than one that does not. Is this rational?

Investment approaches whose underlying premise is to build a replacement income stream through dividends is underpinned by this behaviour. We’ve written previously about these approaches noting they simply narrow the investment opportunity set restricting risk exposure to larger, higher dividend paying securities.[1]

While we understand the psychological benefit of receiving an income stream that would fund your retirement without having to sell down on capital, there are some underlying pitfalls with this thought process.

This has been outlined in “The Dividend Disconnect,” a paper published in the Journal of Finance.[2]

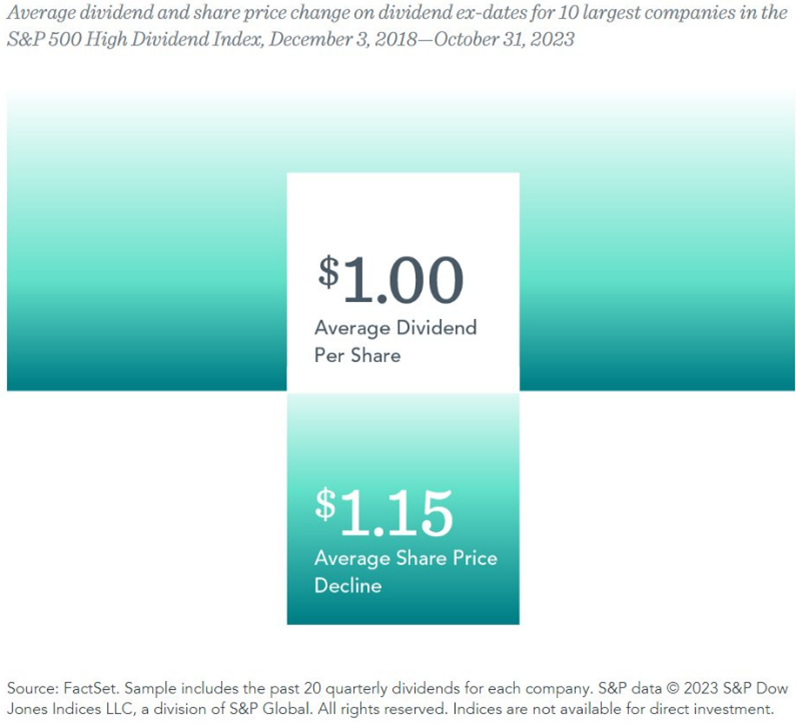

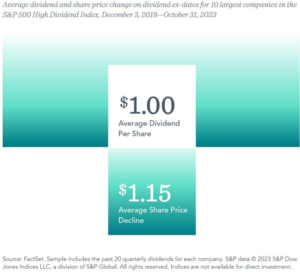

This suggests dividends are not investment returns, nor do they offer any kind of downside protection or hedge when markets are flat or falling. Prof Samuel Hartzmark (author) suggests dividends should be viewed like moving money from one pocket to the other.

“If you view a dividend as separate then all of a sudden you can view this as kind of a stable asset that is uncorrelated with the price level of the stock. But because the dividend payment comes out of the price level it’s not a hedge at all. It would be like saying, okay I’ve got $10 in my right pocket and I’m going to put a dollar bill in my left pocket and now I’ve hedged something. But no, you’ve still got the $10. So, it appears that way, but it really isn’t.”

This is known as the “free dividends fallacy”.

Standard models in finance suggest that value maximising investors should treat all money equally, irrespective of source. Accordingly, dividends should be irrelevant to investors. It’s simply an exchange of capital for income.

This is not to suggest you should avoid companies that pay dividends. It’s to recognise the total return of the company does not change simply because they pay part of that return as dividends.

In Australia, our tax system favours capital distribution over dividends, with tax discounts available for capital gains. So, selling down capital offers a more tax efficient source of cash than dividends. And while many will argue the benefits of franking credits, there is no economic advantage of dividends paid from either franked or unfranked sources. See Franked dividends and your investment strategy – Wealth Foundations and Dividend imputation and super funds: debunking the myth – Wealth Foundations.

Yes, it can be argued dividend paying shares can outperform, but the dividends themselves are not the causal factor. Shares with high yields that grow their dividends tend to be shares with low relative price (i.e. value), high profitability and conservative investment exposure. These recognised asset pricing factors explain the performance variation, (not the dividend policy) and should be the focus when building portfolio structures.

And while the psychology that attracts more buyers to a dividend paying share will likely increase its price, this isn’t a valid reason to buy the share. This increases the price for no economic reason, which simply lowers your expected return. In other words, you end up paying more for the same expected return from a dividend paying share than a non-dividend paying share.

Investors love of dividends is a little more illusory appreciated and can add cost and inefficiencies to an investment approach. Focusing on well researched, reliable risk factors helps remove this bias and offers more efficient portfolio outcomes.

[1] The Great Dividend Yield Chase – Wealth Foundations

[2] “The Dividend Disconnect,” by Samuel M. Hartzmark and David H. Solomon, published in Journal of Finance, Vol. 74, No. 5 (October 2019).