It’s maintaining real spending power that matters

When clients consider how much they expect or wish to spend in the future, they naturally think about it in terms of today’s dollars. The implicit assumption is they don’t want price inflation to erode the amount of goods and services they are able to purchase.

In our cash flow modelling, we assume an inflation rate of 2.5% p.a., mid-way between the Reserve Bank’s target of 2-3% p.a.. With inflation at 2.5% p.a., the spending power of a $1 would be reduced to about 48 cents over a thirty year period.

So, while a financial projection that shows your investment wealth grows from, say, $1 million now to $2 million in 30 years’ time may appear impressive, after adjustment for inflation of 2.5% p.a. the future $2 million is only worth $953,000 in today’s terms i.e. you’ve actually gone backwards in spending power.

While we are very focused on after-inflation, or “real” projections for our clients, it’s not a straightforward matter to choose an appropriate measure of inflation, for modelling purposes. The reality is that given every client’s spending patterns are different, the inflation each experiences will also be different.

To simplify things, we assume that the All Groups Consumer Price Index, Australia (“CPI”), published quarterly by the Australian Bureau of Statistics, is the best indicator of changes in retail prices experienced by our clients. But given that it is a “representative” weighted average of the prices of many items, across eight capital cities, it’s likely that it may not reflect anyone’s inflation reality.

The rest of the article drills down a little into the CPI construction, with the aim of helping both clients and other readers reconcile their sense of what is happening to prices and the headline CPI inflation rate that the media focuses on.

Broad inflation measures capture the “average” inflation experience

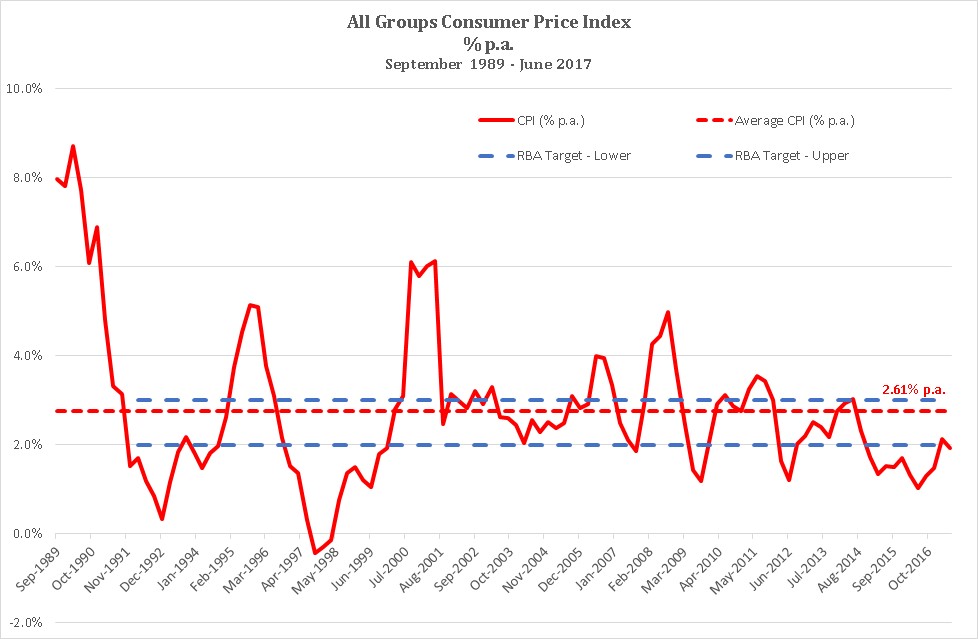

The chart below shows annual changes in the CPI since September 1989 to June 2017, together with the average for the period and the RBA target inflation bands (inflation targeting began in the early 1990s).

Based on the more recent experience, the assumption of 2.5% p.a. inflation used in our projections appears reasonable.

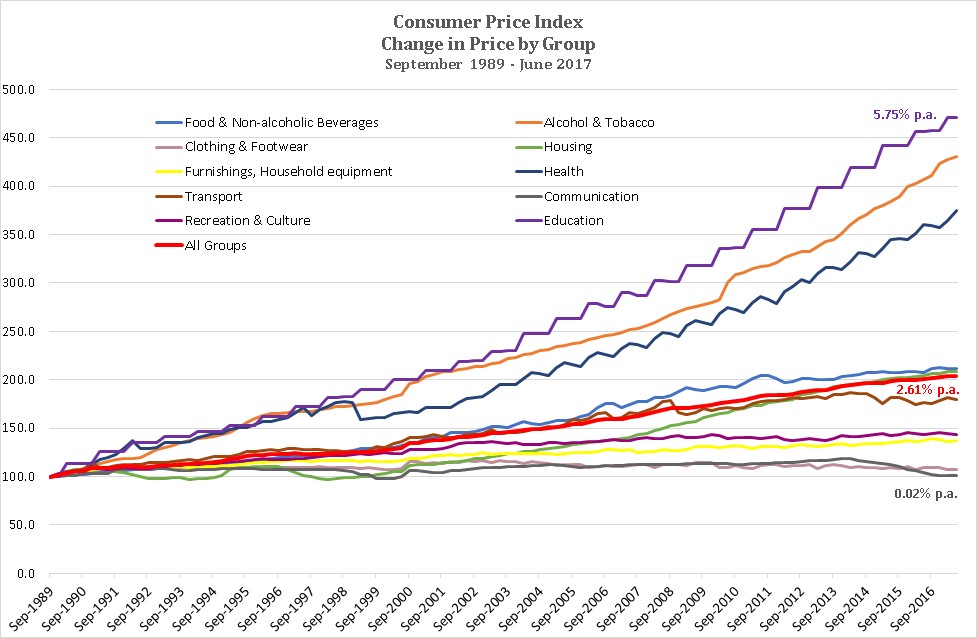

The CPI, charted above, is a weighted average of the price movements of number of major commodity groups, or categories, which themselves are broken down into subgroups and expenditure classes. The cumulative price movements for most of the commodity groups are graphed below and compared with the cumulative movement in the All Groups Index:

The prices of a number of commodity groups (e.g. Education, Health and Alcohol & Tobacco) rose much more than “average”, while others (e.g. Communication, Clothing & Footwear) were virtually stagnant over the almost 28 year period. Clearly, a person whose expenditure pattern was more heavily weighted (than the representative pattern used to calculate the CPI) to health/education/alcohol & tobacco would have a much different perception (and experience) of inflation than another who was more heavily weighted to communication/clothing & footwear.

A potential surprise revealed in the chart is that the price of housing services (the green line) rose roughly in line with average inflation over the period examined. For those in Sydney and Melbourne, given our recent experience with any prices associated with housing, this defies logic.

The primary explanation for the disconnect is that movements in the price of land (the main driver of movements in the prices of dwellings) are excluded from the CPI. Land is regarded as investment (or non-consumable) rather than consumption spending. The CPI measure attempts to capture changes in the price of housing related services and home building (i.e. things that are consumed).

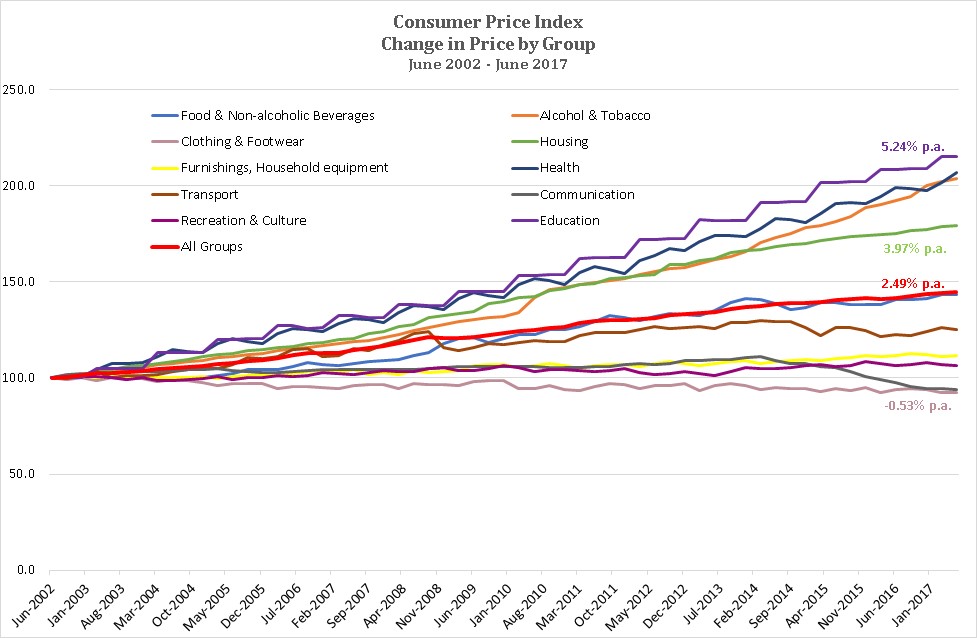

Also, consistently above average inflation rises in housing services are a relatively recent experience, as revealed in the chart below. It shows the same cumulative price movements in the commodity groups as above, but for the 15 years from June 2002:

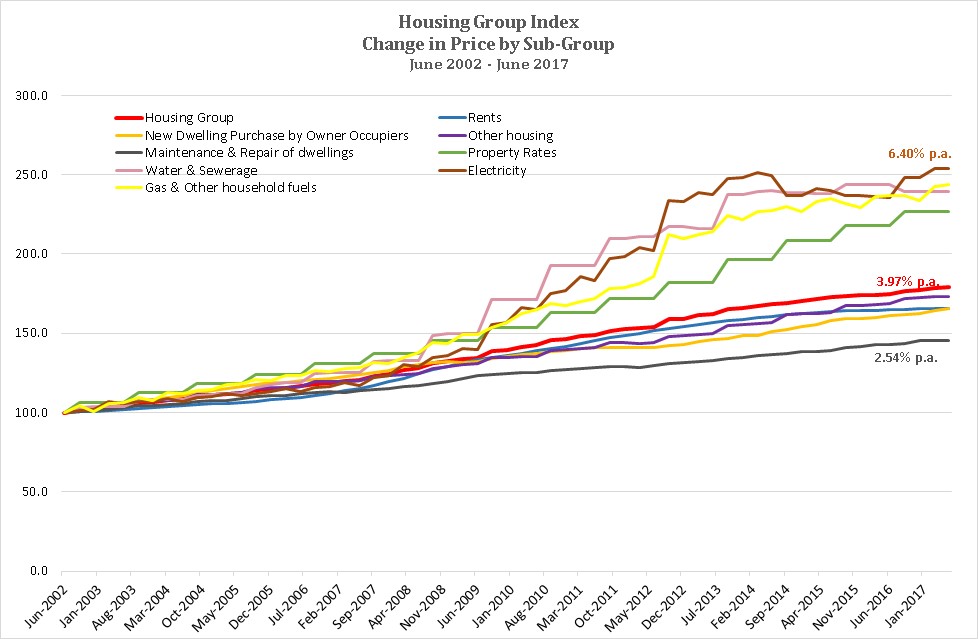

When the housing group index is broken down into its subgroups – see chart below – it’s revealed that utilities (i.e. electricity, gas and water & sewerage) are major contributors to the above average inflation price growth. This is consistent with most people’s experience and is behind the often expressed concern that prices are increasing faster than the headline CPI indicates. But in terms of their current weighting in the CPI, these items only make up about 4.4% of average household spending!

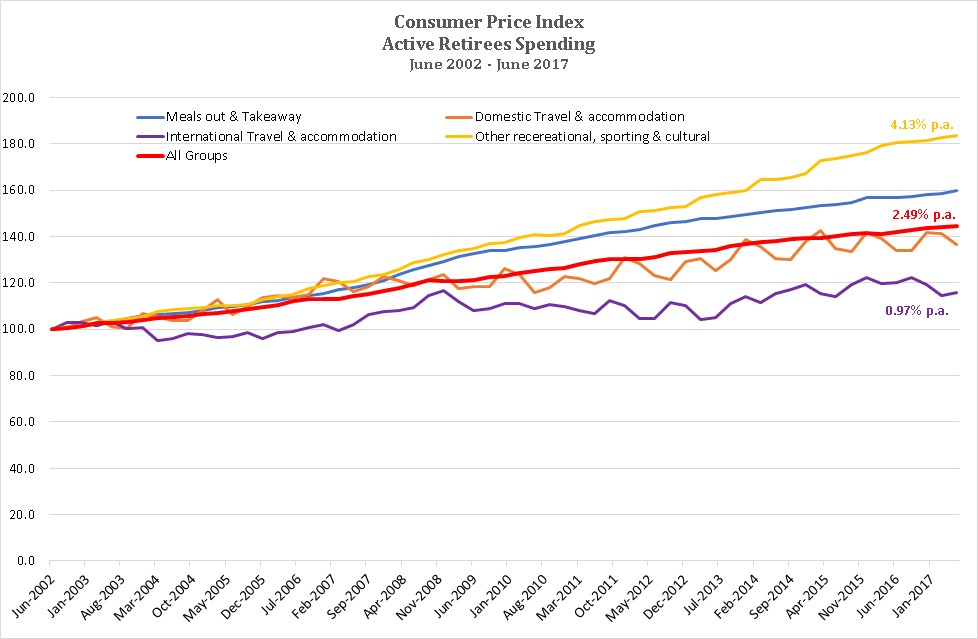

As a final dive into the CPI, we also examined how the prices of some goods and services that affluent, active retirees tend to purchase relatively more of (e.g. travel, eating out, attending sporting and cultural events) moved compared with average inflation. The results are provided below for the period since June 2002:

Preservation of real spending can’t be guaranteed, but ignore inflation at your peril

Although hardly rigorous, there’s nothing to suggest from the small sample above that affluent, active retirees face greater than average inflationary pressures. However, as retirees become less active and more unhealthy, spending on health could be expected to take a greater share of household spending, implying a higher inflationary experience than average.

We take some account of historically rising health costs in our cash flow projections by assuming both medical expenses and health insurance rise at a rate of 3% p.a. above average inflation. Also, given the historical above average rises in education spending, we again assume growth of 3% p.a. above the average inflation rate.

We acknowledge that our broad brushed attempts to ensure clients preserve their real spending power have shortcomings. But, unless cash flows and investment returns methodically, even if imperfectly, take inflation into account, the worth of any financial planning projection is questionable.