Emerging markets have recently re-emerged

The two years to end December 2017 saw the MSCI Emerging Markets index (the most widely used benchmark for emerging market shares) massively outperform the MSCI World Index (the benchmark for developed market shares). Emerging markets recorded an annualised return of 19.2% p.a. for the period, compared with 10.8% p.a. for developed markets.

This stellar performance has escaped the attention of many, perhaps because the previous five years saw very lacklustre relative returns for emerging markets. They returned only 2.0% p.a. compared with developed market returns of 15.4% p.a. for the period from December 2010 to December 2015.

Soon after the worst of the Global Financial Crisis, many subsequently disappointed investors jumped onto the story that the future belonged to emerging markets – remember the BRIC excitement (i.e. Brazil, Russia, India and China) – with prospects for developed economies generally assessed as bleak.

But, as often is the case, the most attractive growth stories don’t translate into the highest future share market returns.

Share market prices very efficiently reflect consensus views of what the future holds. The outperformance of emerging markets versus developed markets for the period from the December 1998 inception date of the MSCI Emerging Markets Index to December 2010 of 9.7% pa. compared with -1.9% p.a. suggest the “growth story” had already been heavily factored into share prices!

The obvious question is whether now is a good time to again look hard at investing in emerging markets. Our usual response to such a question in the past has been that, as an asset class, emerging markets offer a higher risk / higher expected return than developed market shares and potential diversification benefits, provided they don’t comprise any more than about 10% of a well-structured portfolio.

However, a recent paper by Ben Johnson of Morningstar, titled “The Evolution of Emerging Markets”, reveals the characteristics of emerging markets are changing rapidly. The rest of this article examines whether these changes warrant a change in our thinking on the place of emerging markets in clients’ portfolios.

Emerging markets are changing

Johnson notes that as at end September 2017, emerging markets shares made up 11.6% of the global stock market, compared with less than 1% thirty years ago. So, they are no longer an oddity but a significant and most likely growing component of global share markets.

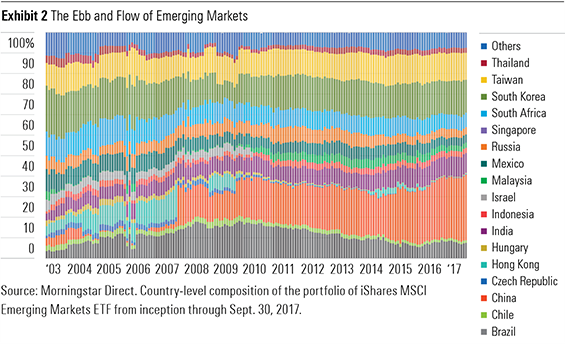

The chart below, copied from Johnson’s article, shows how country weightings of total emerging market capitalisation have changed since 2003.

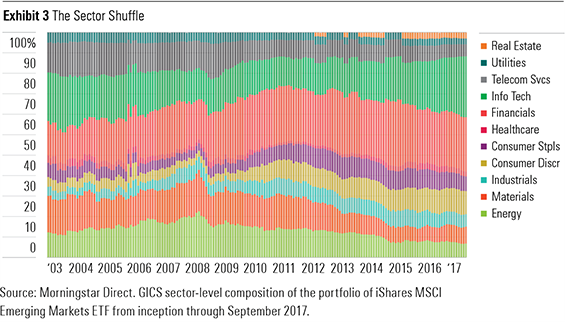

The growth of China and the fall of Brazil, since the peak of the commodity boom in about 2010, is apparent. The change in sectoral composition charted below reveals the rise in energy and materials shares to around 2008 with other sectors, particularly information technology, now becoming increasingly more important.

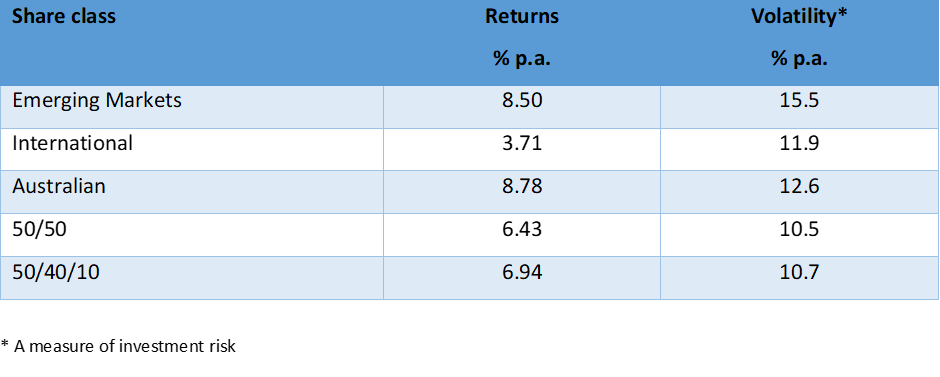

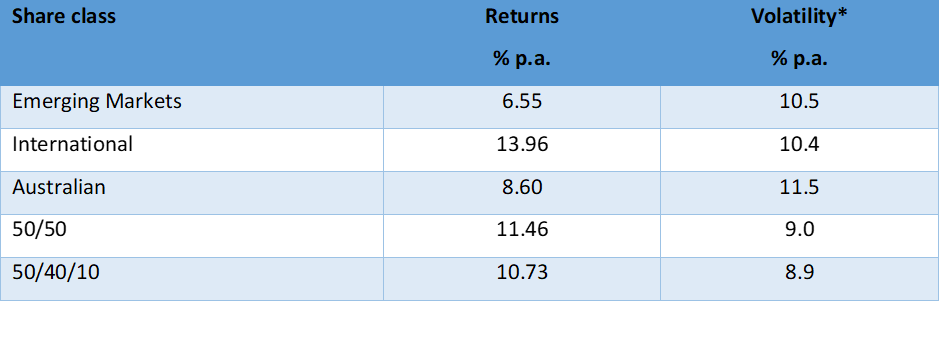

The table below compares the annual return and volatility (a proxy for investment risk) data for emerging markets, international and Australian shares, for the period 31 December 1998 to 31 December 2017. It also provides this information for a 50%/50% weighted Australian and international share portfolio and a 50%/40%/10% weighted Australian, international and emerging markets portfolio:

31 December 1998 – 31 December 2017

The data reinforce the high return/high risk view of emerging markets. The diversification benefit of adding 10% emerging market exposure to an equally weighted Australian and international share portfolio is also revealed, with a significant return uplift resulting with only a small rise in volatility. It appears that our longstanding view on emerging markets as an asset class is supported.

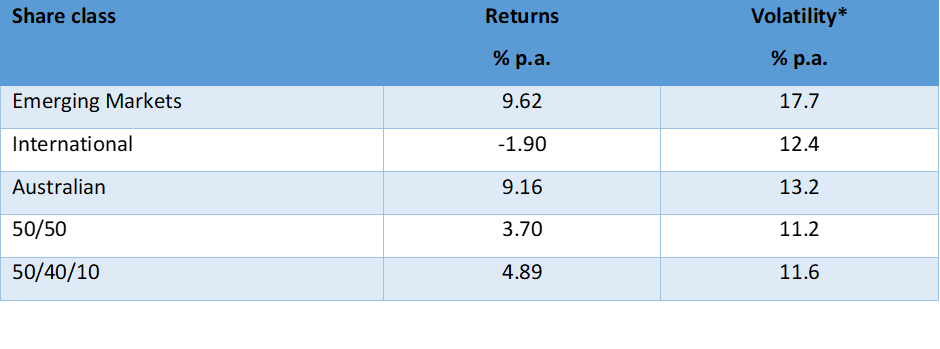

However, when the data period is broken down into two periods – the period from 31 December 1998 to 31 December 2010 and the period from 31 December 2010 to 31 December 2017 – a more ambiguous picture emerges, as shown in the tables below:

31 December 1998 – 31 December 2010

31 December 2010 – 31 December 2017

While the first period provides strong support for adding emerging markets to a share portfolio, taken at face value the past seven years suggests that the asset class is no longer a high return/high risk proposition, having little impact on the portfolio’s risk and, at least for the period examined, worsening portfolio return.

Despite the changes in emerging markets, our portfolio advice will not change … for now

The experience of the more recent data period is far too short to form any reliable conclusions. But with the increasing maturity of emerging markets and sectoral weightings that increasingly reflect global weightings (as opposed to a previous overweighting to materials and energy), it would not be surprising if the return/risk characteristics of the asset class are changing and will continue to change.

Ultimately, there may not be any additional diversification (i.e. volatility reduction) benefit from holding emerging markets exposure over and above that from holding just Australian and international shares. However, given both the likely growing share of global share markets and the expectation of higher returns reflecting higher risk, we continue to remain comfortable with more risk tolerant clients directing up to 10% of their portfolios to emerging markets.